What are PRBs?

The Post-Retirement Benefit (PRB) program allows Canadians who are over 60, receiving the CPP but still working and contributing to the CPP, to receive additional benefits for their contributions.

The program started in 2012 and the first PRB payments were made in 2013.

Before the PRB program started, once you started receiving CPP retirement benefits, you could no longer contribute to the CPP. Now:

• If you are between 60 and 65 years old, receiving CPP, and still working, you must contribute to the CPP.

• If you are between 65 and 70 years old, receiving CPP, and still working, you can choose whether to contribute. (To stop contributing, you must fill out Canada Revenue Agency's Election to Stop Contributing to the Canada Pension Plan form.) Here's the form to restart CPP contributions Election to Restart CCP contributions.

Between age 60 and 70, if you are receiving CPP, working, and contributing to the CPP, you will earn a PRB for each year of your contributions.

How do I get a PRB?

You don't need to apply for a PRB; you will automatically receive it the year following your year of contributions as long as you file an income tax return. Your PRB is effective in January but you may not receive the payment until April or May, with a retroactive payment to January.

The PRB will be added to your monthly CPP pension, even if you are already receiving the maximum CPP retirement amount. The PRB payments will continue for the rest of your life. They are indexed to the cost of living, the same as the CPP.

Each additional year that you continue working and contributing after you start collecting CPP will earn you a new PRB that will be added to your monthly CPP benefit the following year.

How much will I receive?

The amount of Post Retirement Benefit that you will receive depends on your earnings and your age.

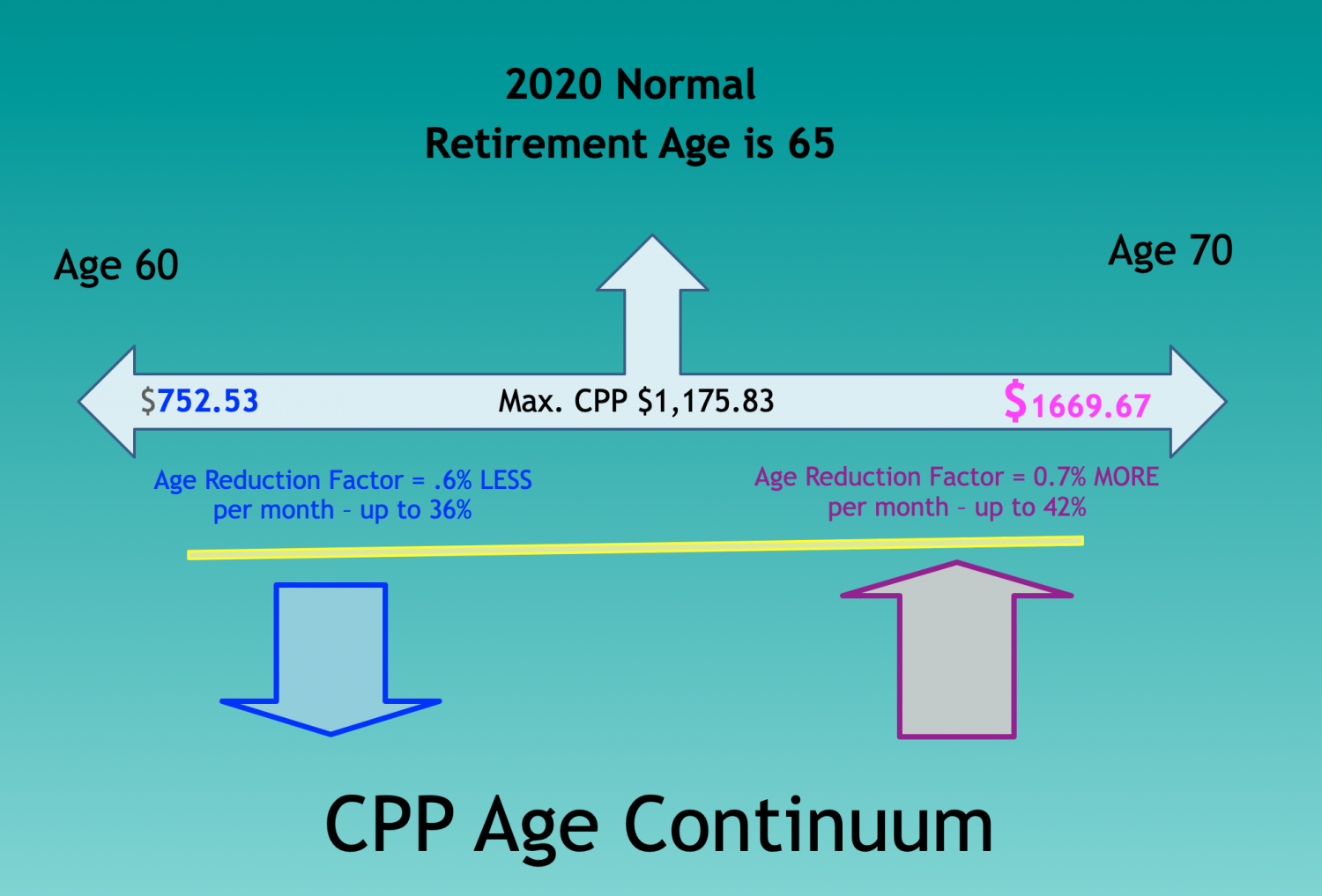

If you are 65, the maximum monthly CPP pension that you can receive in 2020 is $1,175.83, and the maximum monthly PRB is about 1/40th of that, or $29.40. The maximum annual PRB is $352.75 ($29.40 X 12)

If you are any age other than 65, PRB amounts are adjusted, in the same way as your regular CPP — reduced before 65 and increased past 65. Below age 65, both CPP and PRBs are reduced by a factor of 7.2 percent per year (.6 percent per month). Above age 65, they are increased by a factor of 8.4 percent per year (.7 percent per month).

How does it compare to my contributions?

Using a maximum contributor as an example, let's look at the numbers.

In 2020, a maximum contributor makes an annual contribution of $2898 to the CPP. (A maximum contributor is a person who earns more than the Year's Maximum Pensionable Earnings (YMPE). For 2020, the YMPE is $58,700.)

If this maximum contributor is 60 years old, and is collecting CPP retirement pension and still working, their CPP contributions will earn PRBs starting at age 61:

• Their first year of contributions earns a PRB of about $251.16 annually, indexed, for life.

• Their second year of contributions earns a PRB of about $276.56 annually, indexed, for life.

• Their third year of contributions earns a PRB of about $301.95 annually, indexed, for life.

• Their fourth year of contributions earns a PRB of about $327.35 annually, indexed, for life.

• Their fifth year of contributions earns a PRB of about $352.75 annually, indexed, for life.

At the end of the fifth year, their total PRBs will be about $1,509.77 annually, indexed, for life.

Their CPP contributions for the five years 60 to 65 would have been $14,490.

In return for these contributions, their CPP will be $1509.77 more each year going forward. If they live for 20 years past age 65, they will receive approximately $30,195 in PRBs, plus what they received during the five years from 60 to 65 (approx. $1,509.77) for a total of $31,705.17.

All numbers are approximate, are for a maximum contributor, and are in 2020 dollars. If you earned less than the maximum YMPE your PRB would be adjusted down proportionately.

For a 65-year-old maximum contributor, the PRB payback is a return of about 13% per year, indexed for life. If a 65-year-old person earned at least $58,700 in 2020 they would be entitled to a PRB of $382.43 during 2021 (age 66).

The math: (Max. age 65 PRB is $352.75 plus (.7%/month increase 12X.7=8.4%) =$29.63 ($29.63 + $352.75 = $382.43

From a risk/return perspective, this person would be earning a very good return on their contribution of $2898. (Maximum PRB of $352.80 divided by maximum CPP contribution of $2,898 = 13.19%.)

To stop contributing

If you are over 65 and want to stop contributing to the CPP, you must complete the Election to Stop Contributing to the Canada Pension Plan form and give a copy to your employer. If you are self-employed, you must complete the appropriate section of the CRA CPP contributions on Self-Employment and Other Earnings and file it with your income tax return.

You can change your mind and start contributing to the CPP again but you are allowed only one change per calendar year.

If you are self-employed you are responsible for both employer and employee contributions. If that is your case, it may not be beneficial. As with all advice, talk with your Advisor to discuss your unique situation.

Read: Are CPP contributions worth it for the incorporated business owner?

We appreciate your feedback.

Let us know what you like or do not like and how we can make the presentation easier to follow. Send us an email: info@langfordfinanfial.ca

Learn more about our retirement planning process for those 55+

Talk to an Expert - book a zoom or phone call to ask specific questions. The cost is $150.

Retirement Income, Investment & Tax Planning

Willis J Langford BA, MA, CFP

Nancy Langford CRS

“Helping you get your total financial house in order and transition into retirement confidently with purpose and peace of mind "

Thanks to drpensions.ca for help with this information.