It's a question we get asked often: Should I take my CPP at age 60 or wait?

The short answer is NO, the long answer is YES. There are too many variables to be considered to be able to make an instant decision on when to start CPP. Once you start, there are only the first 12 months to reverse your decision. It's a lot of work to stop the payments and you have to repay what you already received. However, if you wait, you can start at any time up to age 70. It's easy to log into your Service Canada account and request that your benefits start immediately.

Consider some of the following in making your decision.

1.) If you are still working, will the additional income bump you into a higher tax bracket? If it does, you may end up losing much of the extra cash. In this case, you may want to wait.

How much longer do you intend to work? How much money do you currently have in other savings? If you do not have a lot of other savings, it may be a good strategy to take the CPP early and invest it in your RRSP, get a tax deduction now and create additional retirement savings in the process. This way, your CPP is creating additional potential income for you that you can use when you eventually retire. One of the best ways to grow retirement savings is by using money that would otherwise be lost in taxes.

2.) Do you have a shortened life expectancy? If you do, take the money now. Start enjoying the benefit as soon as possible because you just don't know how long you will be around to enjoy it. If you don't need the money to live on, invest and grow it so that when you do need it there's more in the pot and more to leave to your heirs. If there's room in your TFSA - sock it away in there.

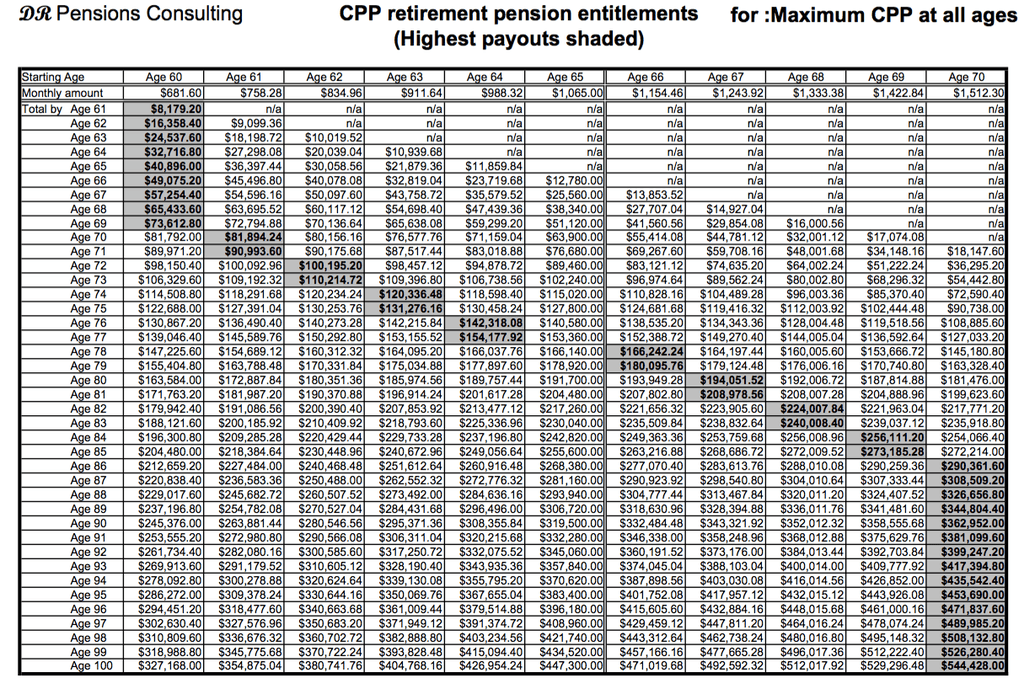

3.) Understand the math. For every month you take your CPP before age 65 you will lose .6% of your CPP benefit. So, if you take it at age 60 that means your cheque will be 36% less than if you wait until age 65. If you delay taking it past age 65 you will earn an additional .7% for each month you delay receiving it.

It seems like a good idea to wait, but before you make a decision consider this: If you compare 3 sisters who are triplets, where Abigail takes the CPP at age 60 and Beth takes it at age 65 and Ella at age 70. The break-even point where Abigail and Beth will both have received the same amount of money is age 74. Ella, on the other hand, will not catch up until age 80. At this point, Ella will begin to outpace her sisters significantly. But keep in mind, she has to have good health and longevity to actually use and enjoy the money. The break-even point shouldn't be the only criteria for your decision. In fact, it should be your last consideration. Taxes, income needs, other investments, size of RRSPs, longevity, and marital status are much more important.

Here's an interesting TABLE that will help you see the differences. (2022 numbers)

|

3 Friends the same age |

Abigail |

Beth |

Ella |

|

Starting Age in 2022 |

60 |

65 |

70 |

|

Monthly Amount |

$801.57 |

$1252.46 |

$1784.17 |

|

At age 65 |

$48,094 |

0 |

0 |

|

At age 70 |

$96,188 |

$75,147 |

0 |

|

At age 74 |

$134,663 |

$135,265 |

$85,640 |

|

At age 81.5 |

$206,805 |

$247,987 |

$246,215 |

|

Life expectancy - age 90 |

$288,565 |

$375,738 |

$428,200 |

Example of 3 brothers with 2018 numbers (Look at how much the numbers have changed over the 4 years)

|

2018 |

Alvin |

Steve |

Mark |

|

Maximum Monthly Cheque |

725.93 |

1134.17 |

1610.52 |

|

Age 65 |

43,555.80 |

0 |

0 |

|

Age 70 |

87111.60 |

68,050.20 |

0 |

|

Age 74 |

121,956.24 |

122,490.36 |

77,304.96 |

|

Age 76.4 |

|

|

122,399.52 |

|

Age 80 |

174,223.20 |

204,150.60 |

193,262.40 |

|

Age 82 |

191,645.52 |

231,370.68 |

231,914.88 |

|

Age 87 |

235,201.32 |

299,420.88 |

328,546.08 |

4.) Post Retirement Benefits. You can only get these PRB's if you are collecting CPP and still working, between the age of 60 - 70. They are significant enough to sway a person to take CPP early. If you have already contributed the maximum to CPP by age 60, (35 years at max. contributions) the additional contributions are not going to add to your CPP. You will only continue to get the age-adjusted increase. If you retire early, let's say at 55, and do not make any more contributions then your CPP is being reduced for every month of delay past age 60.

Deciding when to take your CPP is an important part of retirement planning. Government benefits make up about 25% of your retirement income so getting it right is very important. Think about this: Earning $100/month in government benefits will equal $30,000 of more retirement income over your lifetime.

There isn't a cookie-cutter approach. It brings up many other questions like can I collect CPP while still working past age 65? If I go back to work can I still pay into CPP and increase my benefit? How does divorce affect my CPP benefit? How is the CPP benefit calculated?

We have put together a 6 part series on Everything you need to know about your government benefits. Sign up with your name and email address in the form above and you'll receive an email every few days with the free content.

Click here to learn more about our flat-fee planning services for those aged 55+.

Talk to an Expert - book a zoom or phone call to ask specific questions.

Retirement Income, Investment & Tax Planning,

Willis J Langford BA, MA, CFP

Nancy Langford CRS

Are CPP Contributions Worth It For the Incorporated Business Owner? Read more....

{kind=link}